Finance Terms Every Entrepreneur Should Know

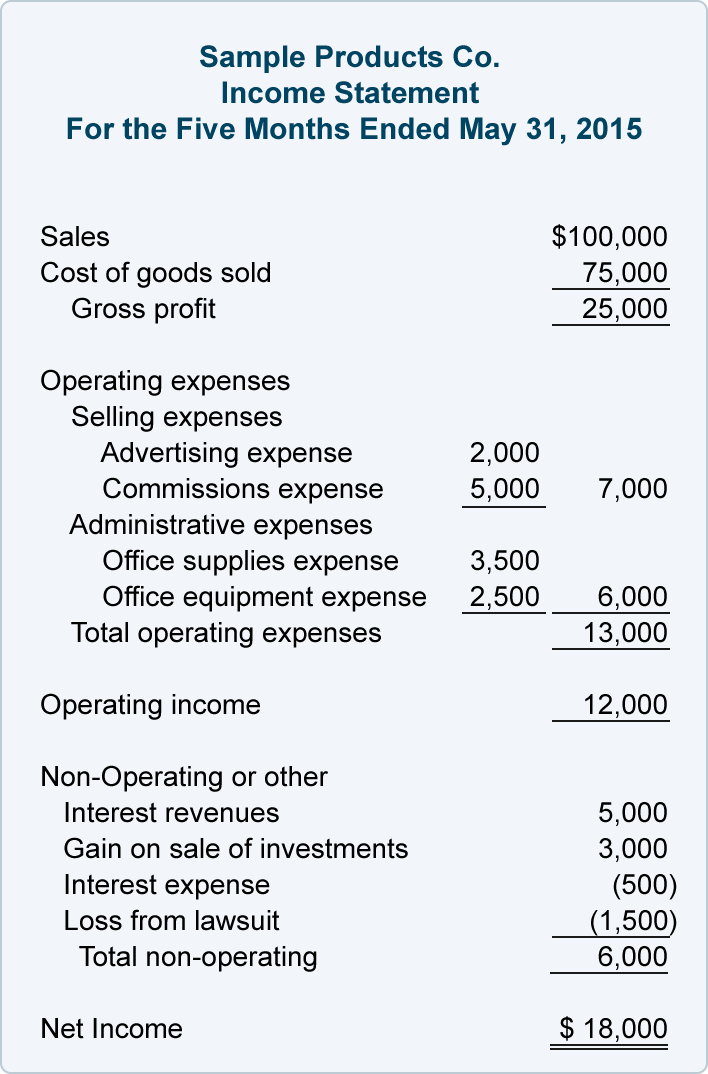

The Income Statement

The income statement is basically a monthly list of all the money that goes in and out of your pocket. Your personal list includes items such as your pay check, plus the money your family gave you, plus debt that a friend just paid back, minus your bank loan, living expenses, bills and every other expense. When it comes to your business, things are almost the same - but there is terminology for the money that goes in and out.

The income statement is an essential financial statement for your business. As mentioned above, It includes your revenue (what you earned from your sales), expenses (what you spent), and the total profit/loss (your revenue minus your expenses). Income statements are important because they demonstrate your company’s ability to operate profitably. When you start running your startup, it is quite easy to lose track of the expenses since there are many unexpected costs and unanticipated losses. To deal with this, try to start drafting your income statement from the very beginning - even before you generate any revenue! This will help with profit-margin calculations and expenditure planning in the future!

Sub-terms: Revenue, Expense, Profit, Loss

Source:http://www.accountingcoach.com

The Bottom Line

What probably matter most on your income statement is the bottom line: the final total which represents your profit/loss, and is often called the ‘net income’ - which is when you earn more than you spend - or ‘net loss’ - which occurs when you spend more than you earn.

Sub-terms: Net profit, Net loss

The Different Types of Profit

When you first start organising your finances, it can be a bit confusing because there are different terms that sound similar, and this is especially true when it comes to profit. It is important to understand the key differences between gross profit, operating profit and net profit.

Gross profit refers to your revenue minus the cost of the goods sold, but it excludes operating costs like wages and rent, as well as overheads such as tax and interest payments.

Operating profit is calculated by minusing operating expenses like office supplies, accounting expenditures and legal fees from the gross profit, and includes additional income other than sales, such as income from investments.

Finally, the net profit includes all income minus all expenses, including operations, overheads and tax.

Some Implicit Costs

Within your income statement, there are some costs that you have to account for, even though you do not explicitly pay for them.

Depreciation can be described as the wear and tear in the value of an asset (mainly machinery) over time.

Amortisation, a similar concept, refers to the routine decrease in value of an intangible asset, for example, a patent.

These two concepts are often difficult to understand because actually they are not real cash outflows. However, for tax reduction purposes, companies write off the amounts from their balance sheets. As a startup, you should understand these concepts as they give you a chance to reduce your costs when paying your taxes. Since your equipment and machinery lose value over time, it means that you won’t be paying the same amount of taxes in the first year and the second year, which can eliminate some of your tax expenditure!

Hopefully this introduction to the income statement will assist you with your business’s financial reporting! It is so important to keep a track of what you spend and earn - doing so will assist you with taxes, credibility to investors and your own financial planning.

Read up more about the income statement:

Introduction to Income Statement